Last Updated on March 7, 2026

Agreements play a crucial role in the construction of residential buildings and apartment complexes, as several legal and financial issues can arise between developers and landowners during the development process. One such agreement commonly used in the real estate sector is the Joint Development Agreement (JDA).

Under the Goods and Services Tax (GST) regime, transactions between the landowner and the developer are treated as taxable supplies, making GST compliance an important consideration in JDAs. However, many landowners are unaware of the GST implications involved in such arrangements.

Therefore, understanding the tax treatment of JDAs is essential to avoid future disputes and compliance issues. This article explains the concept of a Joint Development Agreement and its GST implications in India.

Joint Development Agreement

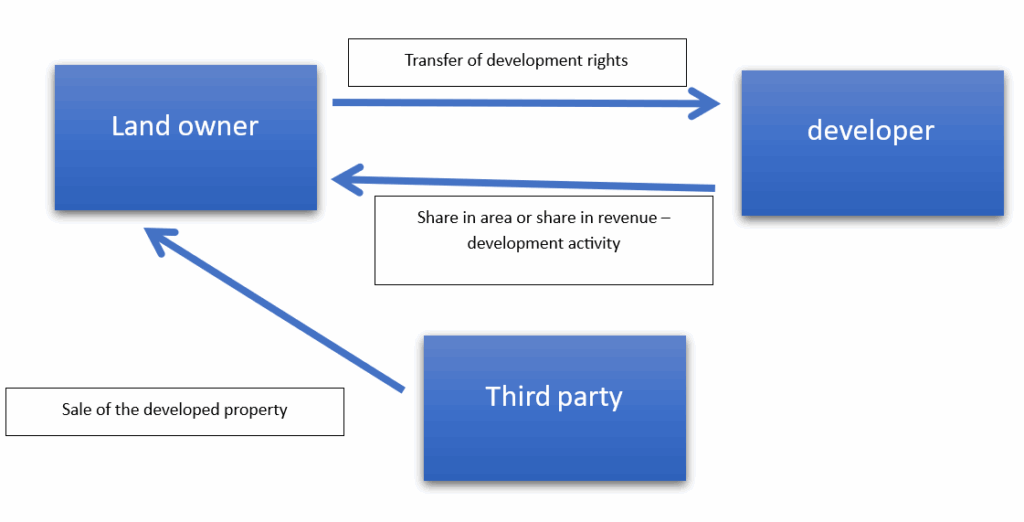

As the name suggests, a Joint Development Agreement (JDA) is an agreement between landowners and developers who jointly develop the property. It is commonly mistaken that the land on which construction is performed belongs to the developer, but this is not always the case; sometimes the land belongs to one party, and the developer enters into agreed terms to develop the building on that land with that party.

How Does a Joint Development Agreement Work?

Let’s assume you plan to build a residential property for sale, but you do not have any land. You will now approach various landowners to procure the land for construction. The landowner will agree to provide the land and the right to construct the property over his land. But what does he want in return? Well, every contract demands the flow of consideration, so do the JDAs. In return, the landowners will require a share in the land, either an area share or a revenue share. But let’s keep in mind that ownership of the land parcel will be held only by the landowners.

Importance of JDAS

Though the term JDA may seem simple, it involves significant complexity, as it clearly lays out the terms and conditions of an investment between parties.

- It facilitates faster development of land.

- Developers may reduce upfront costs associated with land acquisition and stamp duty.

- The landowners provide the builder with encumbrance-free property, and they manage all clearance issues.

- No initial investment is required by the developer.

- It helps the developer obtain loans or create a charge over land that forms part of the JDA.

- It refers to the share ratio of landowners’ land post-construction, as mentioned in the JDA.

Typical Terms of the JDAs

A common JDA will cover the following terms and conditions:

- Details of both parties- the developer and the landowners

- Details of the land premises

- Tracing of the title on the land premises

- Rights/responsibilities of both parties- this will cover

- License rights

- Development rights

- The right to seek approvals from third parties

- Right to take legal action.

- Revenue share/Area share details

- General clauses

- Details of the security deposit

- Sharing ratio-post construction

- Project timeline

- Project specifications: annexures cover construction terms, materials, quality standards, and necessary licenses.

- Legal clauses- indemnification, NDAs, registration details, compensation clauses, etc

- Termination clause

- Taxation clause- GST, TDS, RERA compliances, capital gains

For further information regarding JDAs or assistance in preparing a JDA, please contact our experienced team.

Types of JDA Models

There are three types of JDA.

| Type | Description |

| Revenue Share Model | The developer and landowner agree to share revenue generated from the sale of developed units in a predetermined ratio. |

| Area Share Model | The developed property is divided between the developer and the landowner according to an agreed share of the constructed area. |

| Hybrid Model | Combines both area share and revenue share models, offering flexibility in risk and profit sharing. |

Implications of GST on The Joint Development Agreement

Under GST, the transfer of development rights (TDR) by the landowner to the developer is treated as a supply of service. In most cases, the developer is liable to pay GST under the reverse charge mechanism (RCM).

To analyse the implications of GST on a joint development agreement, it is necessary to address the topic methodically:

- Projects intended for sale – residential and commercial

- Projects not intended for sale – commercial.

Projects intended for sale- residential property

| Transaction | Particulars | Area share | Revenue share |

| Transfer of development rights | Who will pay the tax | Developer | Developer |

| When to pay | In the taxation period, not later than or On The Day Occupancy Certificate (OC) or Completion Certificate Is Issued. (CC) | Up to the date of OC/CC | |

| Value of the tax payable | Deemed to be equal to the value of similar apartments in the nearby areas. | Actual revenue share of sold units upto the date of OC/CC plus the esti,ated revenue share receivable on unsold units | |

| Exemptions | Value exempted to the proportionate carpet area of units sold before OC/CC | Proportionate to units sold before the date of OC/CC | |

| Input tax credit | Not available in the hands of the developer | Not available in the hands of the developer | |

| Tax rate | 18% under the HSN Code | 1% to 5% of the value of unsold units as on the date of OC/CC | |

| Construction services | Who will pay the tax | Developer | No provisions for construction services in the revenue share Joint Development Agreements |

| When to pay | In the taxation period, not later than or On The Day Occupancy Certificate (OC) or Completion Certificate Is Issued. (CC) | ||

| Value of the tax payable | Deemed to be equal to the total amount charged for a similar apartment in the project from the independent buyer. | ||

| Exemptions | Value exempted to the proportionate carpet area of units sold before OC/CC | ||

| Input tax credit | Not available in the hands of the developer. Landowners can claim | ||

| Tax rate | 1.5% / 7.5% as the case under the HSN Code |

Projects intended for sale- commercial property

| Transaction | Particulars | Area share | Revenue share |

| Transfer of development rights | Who will pay the tax | Developer | Developer |

| When to pay | In the taxation period, not later than or On The Day Occupancy Certificate (OC) or Completion Certificate Is Issued. (CC) | No deferment benefit available | |

| Value of the tax payable | Deemed to be equal to the value of similar apartments in the nearby areas. | ||

| Exemptions | No exemption | No exemption for units sold prior to the date of OC/CC | |

| Input tax credit | eligible | eligible | |

| Tax rate | |||

| Construction services | No provisions for construction services in the revenue share Joint Development Agreements | ||

Projects not intended for sale- commercial property (area share)

| Particulars | Transfer of development rights | Construction services |

| Who will pay the tax | Land owner | Developer |

| Value of the tax payable | As per the valuation rule | As per the valuation rule |

| Input tax credit | Not available as on date. | Not available |

| Tax rate | 18% under the HSN Code | 18% under the HSN Code |

GST on Transfer of Development Rights (TDR)

Residential Property

- Before April 2019 – 18% GST applicable

- From April 2019 onwards:

- 1% GST for affordable housing

- 5% GST for non-affordable housing

Commercial Property

- GST rate remains 18%, both before and after April 2019.

Conclusion

Understanding GST implications in Joint Development Agreements is essential for both developers and landowners to ensure proper tax compliance and avoid legal complications. Professional guidance can help structure the agreement correctly and manage GST obligations efficiently.

How Can Kanakkupillai Assist?

Kanakkupillai offers expert assistance in drafting Joint Development Agreements and ensuring GST compliance for real estate transactions. Our team supports developers and landowners with GST registration, GST return filing, and understanding tax liabilities, applicable GST rates, and documentation requirements to ensure smooth and compliant project execution.

Frequently Asked Question

1. Is it mandatory to register a Joint Development Agreement (JDA)?

Yes. A Joint Development Agreement must generally be registered under the Registration Act to make it legally valid and enforceable.

2. When do we have to pay GST on JDA?

As per the notifications and based on the models—area, revenue, or hybrid. In all cases, GST must be paid before or on the date of issuance of OC/CC as per the JDA.

3. Can the owner sell property in JDAs?

Yes, it depends on which JDA you choose. Contact us to learn more.

4. Who is the absolute owner of the land in case of JDA?

The landowner remains the legal owner of the land unless ownership is transferred through a registered conveyance.

5. What is the consideration paid to the landowner?

Area share or revenue share as per the agreed terms.

6. Do we need expert help drafting the JDA, or can I do it myself?

It is always advisable to get expert help.